Media Summary: Unlock the secrets of financial risk management with Ryan O'Connell, CFA, FRM, as he dives deep into Conditional Value at Risk is illustrated for a Hello Candidates, In this video we will be talking about the concept of

Cvar Expected Shortfall Portfolio - Detailed Analysis & Overview

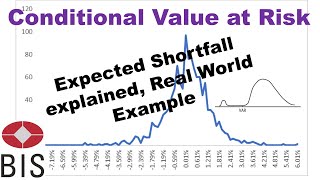

Unlock the secrets of financial risk management with Ryan O'Connell, CFA, FRM, as he dives deep into Conditional Value at Risk is illustrated for a Hello Candidates, In this video we will be talking about the concept of Financial education for everyone Mastering Conditional Value-at-Risk ( In this Video we willl understand all the key concepts about How to address the limitations of value-at-risk? One of the most famous techniques used to measure

Module 5 1 Probability Models for Portfolio Return and Risk ES is a complement to value at risk (VaR). ES is the average loss in the tail; i.e., the This video first explains Value at Risk and then explain the logic and formula of Using the ARMS VaR-engine and the built-in non-linear solver (Downhill-Simplex using Simulated Annealing) we can calculate ... I this weeks class we learn about Conditional Value at Risk and Stress Testing. These classes are all based on the book Trading ...