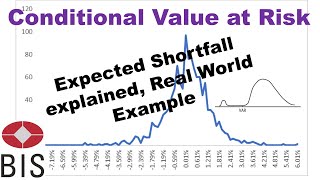

Media Summary: Unlock the secrets of financial risk management with Ryan O'Connell, CFA, FRM, as he dives deep into Hello Candidates, In this video we will be talking about the concept of ES is a complement to value at risk (VaR). ES is the average loss in the tail; i.e., the

Cvar Expected Shortfall - Detailed Analysis & Overview

Unlock the secrets of financial risk management with Ryan O'Connell, CFA, FRM, as he dives deep into Hello Candidates, In this video we will be talking about the concept of ES is a complement to value at risk (VaR). ES is the average loss in the tail; i.e., the Designed for CFA and FRM Part 1 candidates, this video clearly and simply explains the Risk Management concepts of Value at ... This video first explains Value at Risk and then explain the logic and formula of Financial education for everyone Mastering Conditional Value-at-Risk (

I this weeks class we learn about Conditional Value at Risk and Stress Testing. These classes are all based on the book Trading ... Conditional Value at Risk is illustrated for a portfolio of five stocks. The return distribution diagram shows VaR and Ryan O'Connell, CFA, FRM explains Value at Risk (VaR) in 5 minutes. He explains how VaR can be calculated using mean and ... Dive into the world of financial risk management with this comprehensive guide to Value at Risk (VaR). Ryan O'Connell, CFA, ... How to address the limitations of value-at-risk? One of the most famous techniques used to measure