Media Summary: Using the ARMS VaR-engine and the built-in non-linear solver (Downhill-Simplex using Simulated Annealing) we can calculate ... Unlock the secrets of financial risk management with Ryan O'Connell, CFA, FRM, as he dives deep into Talk by Nathan Benedetto in the Combinatorial Optimization Reading Group at University of Waterloo. Abstract: The mean and ...

Quantlab Optimal Hedges For Minimizing Expected Shortfall - Detailed Analysis & Overview

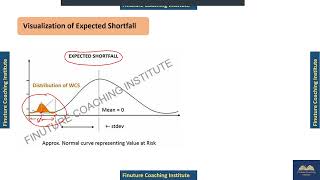

Using the ARMS VaR-engine and the built-in non-linear solver (Downhill-Simplex using Simulated Annealing) we can calculate ... Unlock the secrets of financial risk management with Ryan O'Connell, CFA, FRM, as he dives deep into Talk by Nathan Benedetto in the Combinatorial Optimization Reading Group at University of Waterloo. Abstract: The mean and ... ES is a complement to value at risk (VaR). ES is the average loss in the tail; i.e., the Hello Candidates, In this video we will be talking about the concept of Platform used to test the futures setups discussed in the video: his win rate was only ...

Hi All, Nice numerical along with concept of Work session for the paper: TAReL: Temporal Adversarial Reconstruction of High Frequency Latent Spaces in Financial Markets ... For serious prediction traders: master dependent and cumulative events (over/under ladders, ranges, spreads) with Qwidgets' ...