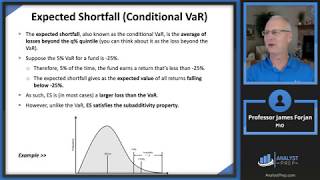

Media Summary: Unlock the secrets of financial risk management with Ryan O'Connell, CFA, FRM, as he dives deep into Hello Candidates, In this video we will be talking about the concept of ES is a complement to value at risk (VaR). ES is the average loss in the tail; i.e., the

Expected Shortfall - Detailed Analysis & Overview

Unlock the secrets of financial risk management with Ryan O'Connell, CFA, FRM, as he dives deep into Hello Candidates, In this video we will be talking about the concept of ES is a complement to value at risk (VaR). ES is the average loss in the tail; i.e., the Financial education for everyone Mastering Conditional Value-at-Risk (CVaR) / Designed for CFA and FRM Part 1 candidates, this video clearly and simply explains the Risk Management concepts of Value at ... Jinghui Chen, University of Toronto and York University September 27, 2024.

In this Video we willl understand all the key concepts about In this Video Sanjay Sir has discussed the basic concept of In this video covers an FRM Part 1 Class, where the instructor explains fundamental topics like VAR, probability distribution, and ... Conditional Value at Risk (CVaR), also known as the In this short video from FRM Part 1 curriculum, we introduce this risk measure In this video from the curriculum of FRM Part 1 and FRM Part 2, we take a look at

In this video, I'm going to show you exactly how we calculate This video first explains Value at Risk and then explain the logic and formula of CVaR, applies 100 day return data of S&P 500 ...