Media Summary: Unlock the secrets of financial risk management with Ryan O'Connell, CFA, FRM, as he dives deep into Expected Shortfall, ... Ryan O'Connell, CFA, FRM explains Value at Risk (VaR) in 5 minutes. He explains how VaR can be calculated using Dive into the world of financial risk management with this comprehensive guide to Value at Risk (VaR). Ryan O'Connell, CFA, ...

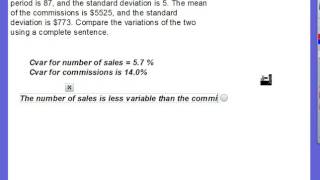

Mean Cvar - Detailed Analysis & Overview

Unlock the secrets of financial risk management with Ryan O'Connell, CFA, FRM, as he dives deep into Expected Shortfall, ... Ryan O'Connell, CFA, FRM explains Value at Risk (VaR) in 5 minutes. He explains how VaR can be calculated using Dive into the world of financial risk management with this comprehensive guide to Value at Risk (VaR). Ryan O'Connell, CFA, ... In this short video from the FRM Part 2 curriculum, we explore the formula for aggregating VaRs computed for each business line ... Ever wondered what Value at Risk (VaR) or Conditional Value at Risk ( I struggled with this concept back at University and I hope this video clears up your understanding. I explain it at a high level ...

Calculate VaR for portfolios of stocks in less than 10 lines of code, use different types of VaR (historical, gaussian, Cornish-Fisher) ... In today's video we follow on from the Monte Carlo Simulation of a Stock Portfolio in Python and calculate the value at risk (VaR) ... Financial education for everyone Mastering Conditional Value-at-Risk ( This is the fourth video going through the open-source fortitudo.tech Python package available at: ... In this hands-on Python coding tutorial, we kick off our Bitcoin risk modeling series by focusing on one of the most important ...