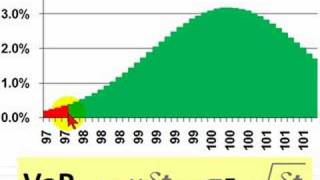

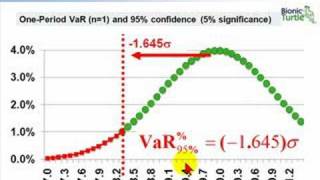

Media Summary: You can get the spreadsheet on our website. The key ideas of this Dive into the world of financial risk management with this comprehensive guide to Here is a quick explanation of parametric

Frm Lognormal Value At Risk Var - Detailed Analysis & Overview

You can get the spreadsheet on our website. The key ideas of this Dive into the world of financial risk management with this comprehensive guide to Here is a quick explanation of parametric Welcome to the first video in this new playlist that is devoted to Topic 5 in the This is a brief introduction to the three basic approaches to In this video we discuss about the Non Parametric Approaches and how they help us to Calculate the

Post Graduate Program In Business Analysis: ... Explore the powerful Monte Carlo Method for calculating SFM Faculty CA Rajeev Ramanath explains a very important concept of Business Analyst Program (Discount Coupon: YTBE15) ...