Media Summary: Ryan O'Connell, CFA, FRM walks through an To know more about CFA/FRM training at FinTree, visit: For more videos visit: ... In this FULL COURSE session on FINANCIAL MODELLING in EXCEL; we have covered everything you need to know about ...

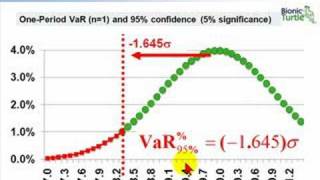

Value At Risk Var Monte Carlo Method Explained - Detailed Analysis & Overview

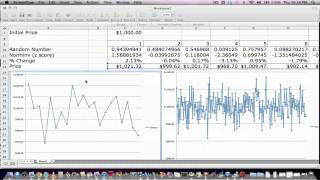

Ryan O'Connell, CFA, FRM walks through an To know more about CFA/FRM training at FinTree, visit: For more videos visit: ... In this FULL COURSE session on FINANCIAL MODELLING in EXCEL; we have covered everything you need to know about ... Today's video provides a conceptual overview of Today we are revisiting the application of basic This is a brief introduction to the three basic approaches to

MattMacarty **Move beyond the constraints of the Normal Distribution!** In this advanced financial modeling