Media Summary: Ryan O'Connell, CFA, FRM explains how to calculate Discover the essential risk management tool, Ryan O'Connell, CFA, FRM walks through an example of how to calculate

Parametric Method Value At Risk Var In Excel - Detailed Analysis & Overview

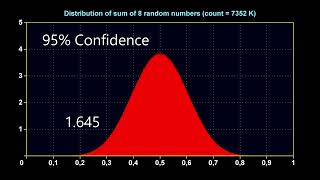

Ryan O'Connell, CFA, FRM explains how to calculate Discover the essential risk management tool, Ryan O'Connell, CFA, FRM walks through an example of how to calculate In this FULL COURSE session on FINANCIAL MODELLING in The key learning outcomes for this episode are: 1) Introduction to So if this are characteristic of my normal distribution and I have 99%

Today we are revisiting the application of basic In today's session, we discuss the concept of confidence levels, significance levels, distribution plot, Normal Distribution, and ... Okay so now we are going to look at how to calculate the MattMacarty **Move beyond the constraints of the Normal Distribution!** In this advanced financial modeling tutorial, you will ...